How to Be Wealthy in Your 20s: The Money Habits of the 1%

Stop wasting money. Discover the exact financial rules and money habits the top 1% use to build massive wealth in their 20s. Start your blueprint today.

The financial plan handed down from the previous generation may no longer be sufficient for success if you're in your 20s. The traditional "save and wait" strategies are now virtually guaranteed to lose ground in an era of skyrocketing rent in major cities such as New York and London and the fact that inflation is eating away at the purchasing power of your hard-earned cash.

You will need more than a raise to become a real millionaire in the real world today; you will need a mindset change about money. It's not about quitting coffee or “clipping coupons.” This means a shift in thinking from consumer to investor.

The Core Difference: Your Dollar Perspective

The difference between the rich and the average man is ALL in their psychology with regard to their disposable income.

- Consumer Mindset: Money is for buying things, status and instant gratification. They always find a new product or service that they wish to purchase when they are granted a raise. They use debt to purchase depreciating liabilities.

- The Wealthy Mindset: Thinks of money as a "worker" that works to create more money. When these people get a lot of money, they seek assets that can generate income. They manage debt well, if at all, and not on lifestyle inflation.

Modern society is designed to make you a lifelong consumer. We see the curated luxury of our peers on social media, we follow targeted ads everywhere, and "Buy Now, Pay Later" apps make it easier than ever to live way, way beyond our means.

Ordinary people spend their money on luxuries first so they can look rich, and this leads them into a kind of poverty. There is a golden rule among the rich: They buy assets first, they buy luxuries last.

Understanding and Using Tax-Advantaged Accounts to Beat Inflation!

It is a futile fight to keep all of your money in a regular checking account. Inflation is an unnoticeable tax. As governments create more money, the value of raw money drops as hard assets, such as stocks and real estate, tend to increase in value.

A liquid emergency fund is a must-have for safety, but your wealth should be invested in assets as soon as possible. The best way to do this is to make use of tax-advantaged accounts.

🇺🇸 If You Are in the United States:

- Roth IRA: Grows your after-tax money completely tax-free, and allows for completely tax-free withdrawals in retirement.

- 401(k): Make at least the minimum contribution to get the matching from your employer. Passing up a company match is literally passing up free money.

🇬🇧 If You Are in the United Kingdom:

- Stocks & Shares ISA: Allows you to invest up to £20,000 per year (as of current limits) completely free of capital gains and dividend taxes.

Here are 3 Financial Goals to Set Before You Turn 30

If you want to have a bulletproof portfolio before you hit your 30s, follow these 3 basic portfolio habits:

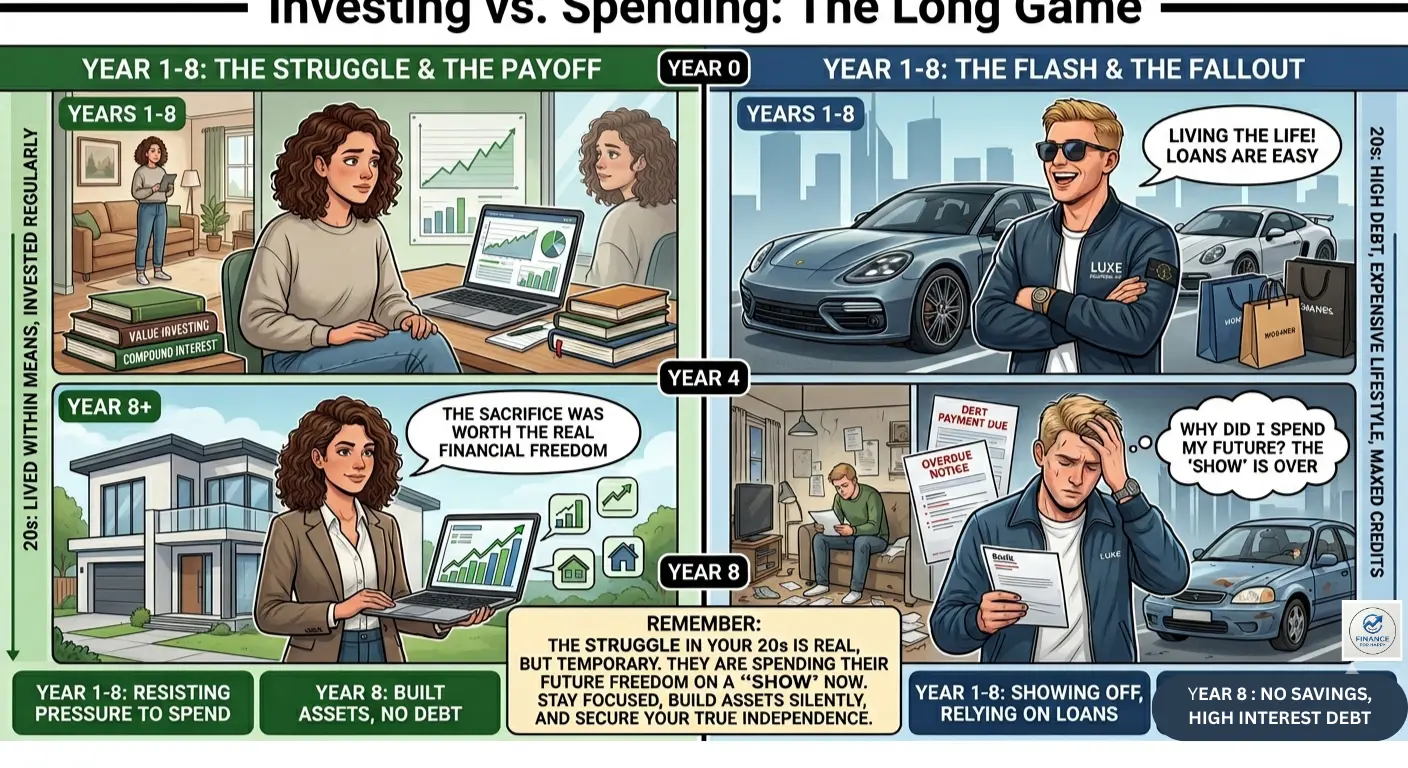

1. Put Your Finances on Autopilot

If you are putting in money-saving efforts on a monthly basis, it is not a good plan. There will always be a surprise trip, an emergency or a good offer. Remove the element of human error by setting up automatic transfers. Make sure you have at least 20% of your paycheck automatically deposited directly into your investment accounts when you are paid. You can't temptation-spend money that you don't have in your checking account.

2. Make a Huge Investment in Your Earning Power

A $1,000 investment that returns 7% in the stock market isn't going to make any difference in a person's life. Your most important asset when you're in your early 20s is your earning power. Buy books, high-dollar skills courses, and certifications that can double or triple your base income. The 10% return for a small portfolio is negligible, while a new skill that helps you get a $20,000 raise means you have a great financial machine to invest in the future.

3. Be at Ease Being "Left Out"

The toughest psychological challenge of becoming wealthy as a youngster is seeing other people drive cars they don't have the money for, wear designer clothing they can't afford, and live in luxurious apartments that they have to pay for. One has to learn to brush it aside. Understand they are sacrificing financial freedom for a short-lived, flaky appearance.

Your Next Steps

Nobody is going to come to save your fiscal destiny. Corporate loyalty is virtually extinct, traditional pensions are disappearing, and of course, inflation is a reality. Financial freedom belongs solely to those who cease to buy and fund other people's businesses and begin to buy and invest in their own future.

📋 The Retail Investor Checklist

Before you log off today, check in your finances with these financial action items:

[ ]Conduct a Spending Audit: For the past 30 days, do a spending audit and categorize purchases. Did you spend your money on things that give you freedom in the future (index funds, stocks, books) or things that give you transient status (luxury clothes, too much eating out)?[ ]Out of Sight, Out of Mind: Remove shopping, fast-fashion, and food delivery apps from your phone to stop impulsive, one-click buys.[ ]Automate Your Wealth: Go onto your bank's website right now and arrange an automatic repeating transfer into your investment account of at least 20 percent of your income for your next payday.[ ]Catch Up on Your Tax Planning: Make sure you have an open and active account that is tax-efficient, such as a Stocks & Shares ISA or a Roth IRA, to safeguard future compounding gains from any unnecessary taxes.

A Final Reality Check: Keep in mind that there is no legitimate way to get rich quick. Building true wealth requires time, discipline, and patience. Every "get-rich-quick" method you chase is almost virtually guaranteed to leave you much poorer than before. Stick to the compounding process.

Stay happy and wealthy,

Finnly Joy.

Now that you have the foundational strategy down, it’s time to put it into practice. If you are ready to build a personalized, wealth-building road map today, dive into our step-by-step blueprint

Disclaimer: The information provided in this article is for educational and informational purposes only and should not be construed as professional financial, investment, or legal advice. Investing involves risk, including the potential loss of principal. Past performance is not indicative of future results. Tax laws vary by jurisdiction and are subject to change. Please consult with a certified financial planner, licensed accountant, or qualified professional before making any major financial decisions.