How an Investing Mindset Can Help You Retire 5 Years Earlier (and Find Your True Happy)

Retirement isn't an age; it’s a financial milestone. By shifting from a "Consumer Mindset" to an "Owner Mindset," you can reclaim five years of your life. This is the ultimate strategy for achieving true financial independence. Start your journey today!

Have you ever found yourself on a Monday morning at work looking at the clock and saying to yourself, "There are still four days left until Friday"? It has happened to all of us. Realistically, for many, the word "retirement" is a foreign concept achieved only when we are too exhausted to enjoy it.

But is retirement an age? It's a number in your bank account plus a specific mindset. This new outlook on investing isn't about saving pennies; it's a reinvestment of five years of your life to do what you really want to do—whether that is writing a novel, starting a boutique business, or traveling the world! In the UK and the USA, retirement is often seen as the end of work. For the “Finance for Happy” community, retirement is all about Financial Independence. It is when you work because you want to, not because you must.

If you can retire 5 years sooner, you'll gain 1,825 days of freedom. You can use that time to scale a digital business or spend it with your family without the shadow of a paycheck looming over your head. The biggest hurdle is not your income; it's your mindset. Most people operate with a "Consumer Mindset"—thinking only of what they can buy today. Successful investors cultivate an "Owner Mindset"—asking themselves, “How much freedom can this dollar buy me?”

The "Status Trap" vs. "Freedom Fund"

| Aspect | Consumer Mindset (The Status Trap) | Investor Mindset (The Freedom Fund) |

| New Income | "I need a better car to match my promotion." | "I can increase my monthly index fund contribution." |

| Market Drops | "Oh no! I'm losing money. I should sell everything!" | "Everything is on sale! Time to buy more assets." |

| Daily Habits | Spending $5 per day on a cup of coffee. | Automating $150 per month into a Roth IRA or ISA. |

| Goal | Looking rich today. | Achieving wealth and freedom tomorrow. |

To shave 5 years off your working life, you need a "three-pronged" approach: frugality, investing, and side hustles. It’s not just one; it’s the synergy of all three! And no, you don't need to live on beans and toast. Strategic frugality involves cutting expenditures on things that don't bring you joy to provide for your future freedom.

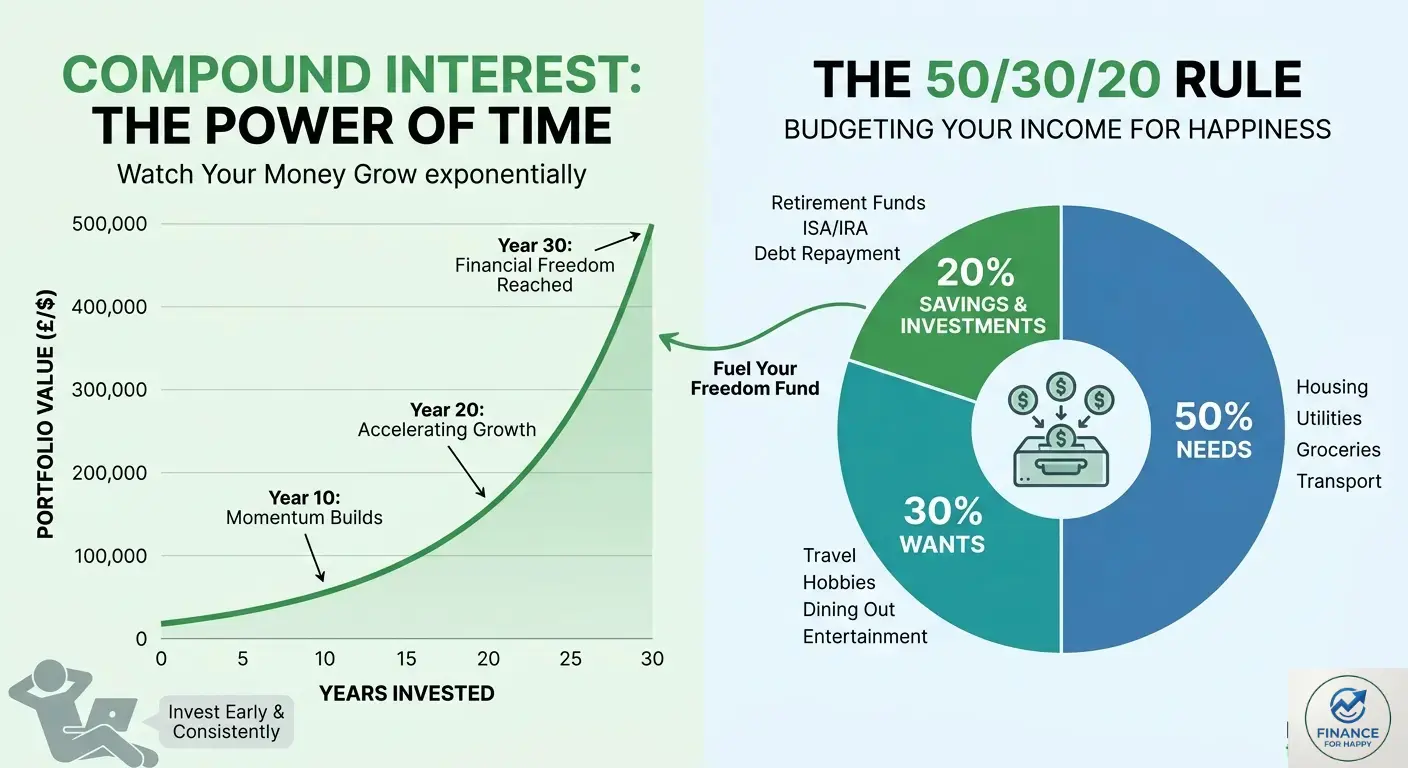

A. The 50/30/20 Rule:

- 50% for Needs: Housing, utilities, and groceries.

- 30% for Wants: This is where your “Happy” comes in—travel, hobbies, and dining.

- 20% for your Freedom Fund: Debt repayment and investments.

B. Compound Interest: Your silent employee. Einstein called it the eighth wonder of the world! Time is your most valuable resource.

C. In the digital world, having just one income is not the safest bet. A side job, like writing, a Ghost CMS blog, or digital marketing that brings in an additional $500 per month can be the deciding factor in whether you retire at 60 or 55.

The most difficult aspect of an investing mentality is the "Waiting Game." 20 years to let investments compound is a long time in the era of 2-day shipping and instant streaming. The brain, however, is malleable. Do not think of it as a "sacrifice" but rather as a "trade." You aren't just skipping a new phone; you're buying two months of freedom. Successful investors are able to keep their heads cool when everyone else is panicking, thanks to this mental shift.

The cost of living has been a factor in everyone's lives in 2026. As prices go up, many people stop investing because they feel poor. But an investor's mindset is to buy assets that can grow in value, such as stocks or real estate. Inflation increases the value of assets and decreases the value of cash.

Avoid “Lifestyle Creep” and other mental pitfalls. Don't raise your spending level along with your income. If you get a $200 raise, put $150 of it right to work in investments. Keep in mind that comparison is the thief of joy; remember that $800 monthly loan payment behind your neighbor's new Tesla. Don't get involved in “get rich quick” schemes and stick with “boring” investing, which is slow and steady growth through an index fund.

Take the time to read your 5-Year Freedom Roadmap:

Year 1: Count every penny. Eliminate high-interest debt. Set up an automatic investment plan.

Year 2-3: Expand your side hustle to cover 10-15% of your expenses.

Year 4: Take advantage of tax-sheltered plans (such as a 401k/IRA in the USA or ISA/SIPP in the UK).

Year 5: Calculate your "Safe Withdrawal Rate" again. You're in the groove now!

Final Thoughts Retiring early is not a matter of luck; it's a matter of strategy. It's the choice to value your time more than any luxury item. You'll never be a slave to the "9 to 5" again once you shift your thinking. Start today. Your future self will thank you while sitting in your own garden or writing that book five years early.

Stay happy and wealthy,

Finnly Joy.

Not sure where to start? [Explore these high-paying side hustles that can fund your freedom fund faster.

Disclaimer

The content on Finance for Happy is for informational purposes only and does not constitute professional financial advice. Investing involves risk. We recommend consulting a certified financial professional before making any investment decisions. Finance for Happy is not liable for any financial losses based on the information provided here.